Written by: Samira Fatehyar

Synopsis

Listen to the podcast version here:

First off, my apologies for the one week delay. If you subscribe to my email list here on my website, you can get updates about new podcast episodes and blog posts straight to your email.

There has been a lot that has occurred over the last three weeks, but that seems to be the way things are going right now. Everything seems to constantly be changing. Anytime I watch the news it baffles me when I see media outlets trying to spin economic data one way or another. It’s hard to look at everything going on with unbiased eyes, but there is a lot of political pressure to spin it one way or another. It’s my hope that my blog and podcast can help people understand what the data means. I’m not persuaded by any political ideology when I research the data. Though I will admit that I have more of a negative view on the economy, hence the title of my podcast is called Bad Bad News. But I stand by the fact that I think it’s better to over-prepared than to be underprepared. As always, I like starting with hard data, so we’ll look at some economic indicators to let us know how things are going. We’ll then dive into a real estate market update. And finally we’ll end with the European View, where this week we’ll be looking at commercial real estate investments being made in Europe and how it compares to the US.

Economic Update

Existing Home Sales and economic fundamentals

We’ll first start by looking at the existing home sales numbers that come from the National Association of Realtors (NAR). There were many headlines over the last two weeks that seems to show that we are on the path to recovery with the new numbers out. This is actually quite worrisome to me, but I will get into why in a little bit. Graph 1, below, shows the total existing homes as a seasonally adjusted annualized rate.

Graph 1

Total Existing Home Sales

https://www.nar.realtor/sites/default/files/documents/ehs-07-2020-summary-2020-08-21.pdf

There was a 24.7% increase from June to July. This is fantastic news, right? Not necessarily. From the graph, it’s telling us that there has been a V-shaped recovery in home sales, which is great. The pandemic has not stopped people from buying homes and in fact has increased to a level we haven’t seen in recent years. But, if we look at the median home price data, we can see that it is still climbing. Graph 2, below, illustrates this.

Graph 2

Median Price of Existing Home Sales

https://www.nar.realtor/sites/default/files/documents/ehs-07-2020-summary-2020-08-21.pdf

People ask, why is it so bad that prices are rising? It’s simple supply and demand, there’s not much of an inventory right now and there is a high demand for homes especially in the suburbs. These are all true facts, it has a lot to do with supply and demand, but the problem is that the demand is not sustainable. As far as I remember, the pandemic has caused record high levels of unemployment, many businesses to fail, and wage growth has substantially remained lower than price growth of homes.

Graph 3

Wage Growth Tracker, Weighted Series

https://www.frbatlanta.org/chcs/wage-growth-tracker

Now, looking at the wage growth tracker above, in Graph 3, we see that wage growth has remained at a decreased level for quite some time now. July 2020 saw a 3.9% wage growth. In a previous post, I showed that in the past 10 years, we have seen home prices increase by about 45-50%. This is not sustainable. And trust me, I know I’ve been saying this for awhile now, but it will only be a matter of time before we realize just how bad this situation is. I’m sure we all know where the unemployment numbers are, but I think it’s always nice to see a visual to highlight the data. Graph 4, below, shows the unemployment rate in the US.

Graph 4

Civilian Unemployment Rate, SA

https://www.bls.gov/charts/employment-situation/civilian-unemployment-rate.htm

According to this graph, the preliminary number for the official unemployment rate is at 10.2%. Granted, it has decreased significantly since the initial shock in March/April, but it’s still higher that the peak we saw during the Great Recession. And yet, home prices are still increasing. Yes, I know interest rates are at an all time low, but the truth is, interest rates will remain low for the foreseeable future. This should add more proof to the case I’m making about the unsustainable market.

I thought it would be interesting to see the Sales Distribution chart provided by the NAR, to better understand what price ranges of homes are selling.

Table 1

Sales Distribution for July 2020

https://www.nar.realtor/sites/default/files/documents/ehs-07-2020-supplemental-data-2020-08-21.pdf

A key takeaway from this chart is that the bulk of the homes being sold in the US in July was in the $100K-$500K range. This, of course, shifts a bit when you look at different region, but for the most part this tends to be true. A good takeaway from this is that if the home is under $500K then there isn’t a need for a jumbo loan, which is actual good news. My biggest concern, is how long can this last? Yes, more and more people are moving to the suburbs and can afford these homes but if the underlying economic fundamentals are telling us a different story, I once again will ask, how can this be sustained? Maybe, I’m completely wrong, and I do hope I am, but just looking at the numbers, I and many other economists can tell you, it doesn’t make sense.

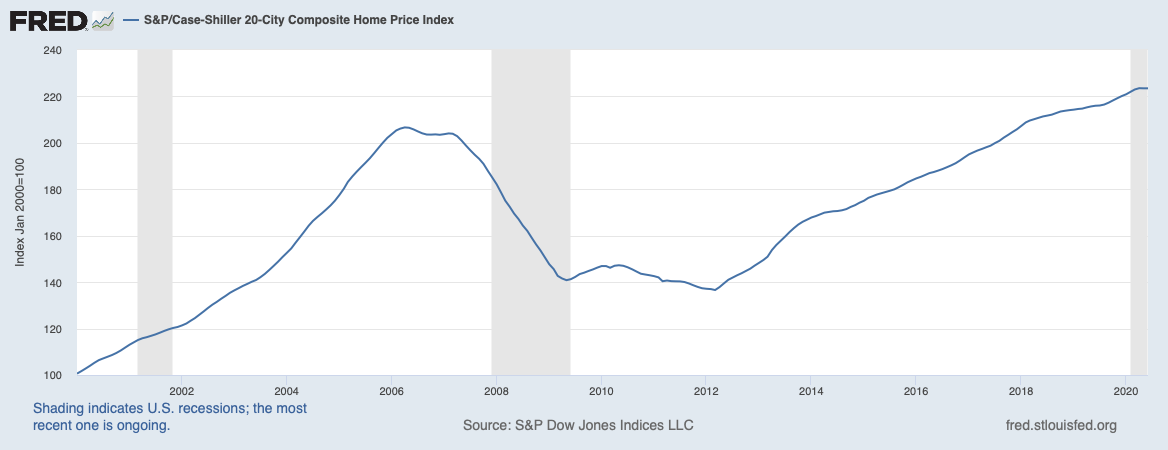

Another important metric to consider is that of the Case-Shiller 20-City Composite Home Price Index, located below on Graph 5.

Graph 5

S&P/ Case-Shiller 20-City Composite Home Price Index

https://fred.stlouisfed.org/series/SPCS20RSA

We are at an all-time high when it comes to home prices and yet we are still seeing our economic fundamentals in very unhealthy territory. We were in an affordability crisis before the pandemic started and yet prices keep rising. What makes us think the affordability crisis will suddenly disappear? Do I think a bubble is forming? I didn’t think so at the beginning, but now I am starting to feel like we might be going in that direction. It’s not the same type of bubble we experienced last time though. This time we are having an exogenous health crisis weakening our already faltering economic fundamentals, but why we are we continuing to see home prices increase? It must be because a bubble is forming.

conference board data

On August 20th, the Conference Board released their new lagging, coincident, and leading economic indicators. Before I dive into what these indicators mean, I think it would first be helpful to understand what the Conference Board is.

The Conference Board is a research group organization dedicated to conducting business management and economic research as well as publishing many widely tracked economic indicators.

Now, let’s define what their lagging, coincident, and leading economic indicators mean.

A lagging economic indicator (LAG) represents changes that happen after the economy changes collectively. It is also used to help confirm an occurrence of an economic turning point.

A coincident economic indicator (CEI) represents the state of the economy at that moment in time.

A leading economic indicator (LEI) represents where the economy is going.

In their recently published report, they highlighted that, “Despite improvement, pace of economic growth will likely weaken in final months of 2020.” The Senior Director of Economic Research at the Conference Board, Ataman Ozyildirim, went on to say that “despite the recent gains in the LEI, which remains fairly broad-based, the initial post-pandemic recovery appears to be losing steam.” Now, before we start getting into what he meant by these words, let’s look at the indicators he is referring to. LEI is a composite index made up of 10 components, according to the Conference Board:

Average weekly hours, manufacturing

Average weekly initial claims for unemployment insurance

Manufacturers’ new orders, consumer goods and materials

ISM Index of New Orders

Manufacturers’ new orders, nondefense capital goods excluding aircraft orders

Building permits, new private housing units

Stock prices, 500 common stocks

Leading Credit Index

Interest rate spread, 10-year Treasure bonds less federal funds

Average consumer expectations for business condition

So, knowing that it is made up of changes in these 10 things, we can now look at Graph 5, below, and understand it a bit more. Graph 6 is the LEI in the logarithmic scale to help show the troughs and peaks more clearly.

Graph 6

LEI on a log scale

https://www.advisorperspectives.com/dshort/updates/2020/08/20/conference-board-leading-economic-index-increased-in-july

Though it looks like we are experiencing a V-shaped recovery, we can look more closely at the last 12 months graph and notice that we are actually decelerating our recovery. This is what Mr. Ozyildirim was trying to convey in his statement in that he is seeing the recovery losing steam. If we were to continue on this track, we could see a further decline, which has happened before and does not necessarily mean Armageddon will occur. Though we should be mindful that there are probably going to be some worse days ahead before better ones arrive.

The CEI is another important indicator as it shows what it occurring right now. The CEI is made up of 4 components, according to the Conference Board:

Employees on nonagricultural payrolls

Personal income less transfer payments

Industrial Production

Manufacturing & Trade Sales

When put the CEI together with the LEI, some economists believe that it can help determine the likely hood of a recession. Though we already know we are currently in a recession, I thought it would still be a good topic to cover. Looking at Graph 7, below, we see the where both indicators have been in relation to each other over the last 20 or so years.

Graph 7

LEI and CEI on a log scale

https://conference-board.org/pdf_free/press/US%20LEI%20PRESS%20RELEASE%20-%20AUGUST%202020.pdf

Now, from this graph it should be easy to see that when LEI > CEI, this usually indicates an expansion and when CEI > LEI, this means that we are experiencing a recession. But what I personally find interesting right now is that it looks like LEI and CEI are both the same and have diverged a bit to now indicate the LEI > CEI, which should mean we are in an expansion, though both are starting to slow down.

I believe it’s important to look at all this data with context. When we look at what both LEI and CEI are made up of, we can make some educated assumptions on where things will probably go in the near future. The components of LEI that I see decreasing will be average weekly hours worked in manufacturing, manufacturer’s new orders, building permits (as winter is coming and usually decreases at this time), leading credit index, and average consumer expectations. What I see increasing is unemployment claims. I also see all 4 components of CEI decreasing as well. The fact is more and more large companies are laying people off, yet many believe our labor market is pretty strong. It’s almost like people are expecting companies to pay employees on borrowed money, but for how long can that be sustainable? The answer is it can’t be for very long. We keep thinking short-term solutions can fix the greater problems at hand and the fact is it can’t. So when we look at these indicators, it seems like things are looking up, but it’s my understanding that we are seeing just a momentary recovery, unfortunately.

Consumer Confidence Index

Another interesting indicator that turned sour in the last few weeks was that of consumer confidence. This data also comes from the Conference Board. It’s hard to say this was a surprise though. Graph 8, below, shows the consumer confidence index since 2011.

Graph 8

Consumer Confidence Index from 2011 to now

https://www.marketwatch.com/story/consumer-confidence-tumbles-to-new-pandemic-low-after-summer-viral-outbreak-2020-08-25

The consumer confidence index is a forward looking indicator in that it looks at how confident consumers are in the future of the economy. As seen in the graph, there was a major dip at the beginning of the year and then a spike last month and now another dip. This is significant and shows how uncertain people feel about the future economy. In addition to this, it was recently reported that Capital One has slashed 1/3 to 2/3 of some people’s credit limits. This will have major ramifications especially for those who have already lost their jobs and are scrambling to make ends meet.

Real Estate Market Update

The last time I did a real estate market update was back in late May/ early June and I thought now would be a good time to see what everything has done since then. Once again, we’ll be looking at REIT data. We’ll first start with the commercial real estate sector and then look into residential.

A quick refresher:

Commercial real estate is essentially made up of retail, office, industrial, multifamily, as well as mixed use. I will separate each sector and talk about them in terms of their REIT returns because that is the most easily available data to analyze the current state of the commercial real estate market.

REITs, or real estate investment trusts, are companies that own, manage, and/or finance income producing properties. These companies have shares that are publicly traded so investors can buy these and receive a dividend without having to actually buy physical property. There are certain requirements to become a REIT, two important criteria include investing at least 75% of total assets into real estate, US treasuries, or cash as well as paying a minimum of 90% of taxable income through shareholder dividends every year. There are also three types of REITs: equity, mortgage, and a hybrid of both.

Nareit is the National Association of Real Estate Investment Trusts. The importance of Nareit is that it publicly provides REIT performance data.

Retail Sector

As we all know, the retail sector took one of the biggest, if not the biggest, hit from the Covid-19 pandemic. When looking at the graphs below, please keep in mind that the year to date numbers I discuss are related to total returns in each REIT category. Table 2-A, below, highlights the returns related to retail.

Table 2-A

FTSE Nareit U.S. Real Estate Index Series Daily Returns as of August 21st, 2020, highlighting Retail

https://www.reit.com/sites/default/files/returns/DomesticReturns.pdf

In comparison, let’s recall the May 28th returns. For retail we saw a -42.62% overall YTD return, shopping centers saw -41.14%, regional malls saw -56.82%, and free standing retail saw a -30.11%. Now when we look at the newer released numbers we see most areas have recovered while shopping centers have actually worsened. I don’t need to go through an extensive list to show you just how dire the situation is, with many retail real estate companies filing for bankruptcy. So although, there has been a slight increase in the year to date returns, all of retail is still VERY negative.

Office Sector

Now if we look at office, we see a very similar story. Table 2-B, below, summarizes the YTD numbers for the office sector. On May 28th, YTD returns for office was -26.14% as compared to now -25.91%. Not much of an improvement.

Table 2-B

FTSE Nareit U.S. Real Estate Index Series Daily Returns as of August 21st, 2020, highlighting Office

https://www.reit.com/sites/default/files/returns/DomesticReturns.pdf

Unfortunately, office and retail seem to be the hardest hit sectors in real estate for obvious reasons. Though, it was known to many of us that retail was undergoing radical changes pre-Covid, it only made it that much worse once Covid happened. With office, there were changes in the making but not as much as retail. Co-working space was starting to take off but many still believed in the traditional use of office space. Thankfully, Covid has changed that and I say thankfully genuinely. I see that Covid has acted as a catalyst for many life-style changes; some of which has really helped the environment. But I’ll talk more on that in a bit.

The main takeaway here is that office is continuing to suffer and probably will as more and more people are being laid off or being forced to work from home. It won’t make sense for companies to rent out office space if many of their employees can easily work remotely.

Industrial Sector

The industrial sector has been quite the anomaly, in that it is outperforming every other real estate sector. This makes sense since online commerce is not only thriving but is the dominating force in commerce right now. Table 2-C, below, highlights the industrial REIT YTD returns.

Table 2-C

FTSE Nareit U.S. Real Estate Index Series Returns as of August 21st, 2020, highlighting Industrial

https://www.reit.com/sites/default/files/returns/DomesticReturns.pdf

For the May 28th, YTD returns, Industrial saw a 0.38% return, Self Storage saw a -6.07% return, and Data Centers saw a 9.82% return. If we compare this to the YTD numbers above we see major improvement in all of the categories. Industrial is thriving in this market. Now you may ask, why is self storage struggling compared to industrial and data centers. A big reason is that there wasn’t as big need for it previously. Though, one reason it is coming back is that many people will have to start downsizing due to being evicted. Americans have a hard time parting with their things and need a place to store important items, so self-storage is the perfect solution.

Multifamily Sector

Now, if we switch to multifamily we see a worsened outlook. On May 28th, we saw YTD returns of apartments at -19.83% while today we see a -24.85%. Table 2-D summarizes these findings. The most obvious explanation for this is the rising evictions and loss of income from these properties.

Table 2-D

FTSE Nareit U.S. Real Estate Index Series Daily Returns as of August 21st, 2020, highlight Multifamily

https://www.reit.com/sites/default/files/returns/DomesticReturns.pdf

Unfortunately, I don’t see this recovering in the short-term. Nevada is set to end its eviction moratorium on Sept. 1st and with that they have estimated that roughly 250,000 in Las Vegas will be evicted and forced on the streets. To put this in perspective, the population of Las Vegas is roughly 645,000. That is almost 40% of the population being affected by this.

I want to emphasis that the problem is much larger than real estate and real estate returns. When that many people become displaced, we’re talking about lasting societal changes. We’re talking about a generation of children that end up living on the streets and aren’t granted the same resources and needs compared to a child with a roof over their head. I wish many in my field would step away from the profits and actually look at the major ramifications that can happen from their profit first driven behavior.

On Saturday the 29th, I saw many videos on Twitter showing lines forming outside of Uhaul as many are in the midst of moving. There is a mass exodus outside of city centers and towards suburbs. Will some of these people return to city centers when the pandemic is over? Possibly a fraction of them, but what we are witnessing is a major shift that will have lasting effects.

Residential Sector

So, all these people are packing up and moving out of city centers, right? If we look at the data below in Table 2-E, we can see that both manufactured homes and single family homes have improved from May 28th numbers. On May 28th, it was reported that YTD returns on manufactured homes was -9.56% and single family homes was -9.76%. Though we are seeing manufactured homes at -3.09% right now, it has improved and I would expect it to breakeven by the end of the year. Single family, on the other hand, has turned positive and will most likely continue as more and more people move to the suburbs.

Table 2-E

FTSE Nareit U.S. Real Estate Index Series Daily Returns as of August 21st, 2020, highlighting Residential

https://www.reit.com/sites/default/files/returns/DomesticReturns.pdf

Though something interesting to note in the table is that home financing is still down for the year at -37.05%. On May 28th, it was reported at -47.77%, which again is an improvement but it is still very negative. So how do we make sense of this? Since interest rates are at all time lows right now, it makes sense that mortgage REITs are also suffering because of this. Furthermore, the returns will most likely remain depressed as long as interests rates remain near zero.

Real Estate’s Future

It’s been interesting to me to see many real estate leaders starting to divide up on what they see happening in the future. I was listening to Jeff Blau, the CEO of Related Companies, go on and on about how he is campaigning for office employees to go back to work in New York City. I’ve learned from many successful people that if you are not willing to adapt to the new future changes you’ll end up losing. One of my mentors, Mr. Ed Friedrichs, former CEO of Gensler, always reminds me that in order to be successful in the business world you need to look at long-term strategies. Long-term strategies requires looking into the future and adapting yourself to change; not resisting the current, but instead adjusting your sails to excel with the flow of things. There’s many opportunities out there to adjust to the future changes coming, but it takes a bit of thinking outside of the box and listening to unconventional ideas maybe from younger people. Unfortunately with the way Mr. Blau is heading, I see a big resistance to change. Instead of being solely focused on profits, he could try stepping outside of his prism and see that there are many other ideas that can make him money as well.

From what I’ve seen from friends working in different industries, is that they prefer working at home than going into an office. The remote work lifestyle was going to come, whether people want to deny that or not, because of the shift in mentality from millennials. Millennials put more of an emphasis on experiences than they do on the accumulation of things. With a remote work life, they can essentially travel anywhere they want to (as long as there is wifi) and still remain productive members of society. So from the workers’ perspective I see many people opting for the remote work life style. But, I also see many people wanting to go somewhere to work, not necessarily at the traditional office but instead in a co-working environment or even tiny offices. We’ve seen the movement of tiny homes taking off, but what about tiny offices? Tiny offices for those that want a private office space away from home and co-working space for those that want the community office environment, but not in the traditional sense.

At the end of the day, it all comes down to the economics of such an idea. The fact is if we move away from the traditional office, companies end up saving a large amount of money and because of the reduced need to travel to work, we’d actually end up reducing carbon emissions. If we were to move co-working spaces and tiny office space to more suburban areas, I think it would not only increase quality of life for people, but would be cost-effective as well as help the environment. What do I mean by increasing quality of life? Well, parents would be able to spend more time with their kids and family then they would having to be stuck in traffic for 2 hours trying to get home. They wouldn’t feel that their life was being wasted during their commute. And in all fairness, not everyone is going to want to be in co-working spaces or tiny offices, when they’d prefer to be at home, but there is a lot of different work styles out there and I think these two ideas would work great for the majority of people. For example, I have a close friend become very upset when her office closed down due to Covid-19 and she was forced to work from home. For the first couple of months it was a pain, but now she is thriving and loves working from home and having flexibility in her life. Of course, not everyone is like this, but it just goes to show that humans can adapt to changes.

European View

This week we will be talking about overall commercial real estate investment in Europe. It was recently reported by Real Capital Analytics that European commercial real estate investment has surpassed that of the US. If we look at Graph 9, below, we can visualize what this means.

Graph 9

Difference between US transaction volume and European volume

https://www.rcanalytics.com/usct-preview-july-2020-mir/

As we can see from Graph 9, the US is in a similar position to that of the start of the Great Recession when looking at the amount of deal activity happening in Europe. So the question is why is Europe looking more attractive than the US for commercial real estate deals? Well as was stated in the Real Capital Analytics analysis:

In mid-August, daily deaths from Covid-19 in the US were nearly 10 times greater than that in the European Union, a region with roughly 120 million more people than the US. With a harder public health situation in the US, investors face greater uncertainty around underwriting future income trends for a property.

An interesting note that they brought up was the fact the US dollar has in fact weakened against the Euro. Traditionally, this should entice more investors from Europe to invest in the US, since their euro can stretch further. But in this instance, we are not seeing that happen. This then leads us to believe that there are bigger risks in the US than there are in the EU. When Real Capital Analytics points out that there is a large amount of uncertainty in trying to identify the underlying value of the property as well as future cash flow, this should read as a red flag. More on these risks in a bit.

Let’s first look at some economic fundamentals in the European Union. Graph 10, below, shows the unemployment rate of the EU over the past 25 years.

Graph 10

EU Unemployment Rate over the past 25 years

https://tradingeconomics.com/european-union/unemployment-rate

The latest stats show us that the unemployment rate in the EU is hovering around 7% as compared to the US which is currently at 10.2%, though it was much higher in the last couple of months. From the graph we can see that the unemployment rate is a bit more stable than the US and that even in the peak of the European Debt Crisis, unemployment was no more than 12%. Granted some countries were hit harder than others, but the same can be said for different states in the US.

Another important metric to consider is that of GDP growth.

Graph 11

EU GDP growth over the past 25 years

https://tradingeconomics.com/european-union/gdp-annual-growth-rate

For a bit of context, Graph 11 is showing an annualized GDP growth rate, meaning that it if things remain the way they are going, the EU economy is expected to shrink at a rate of 14.4%. This is big, I will not disagree with that. But when you compare this with our annualized number of 31.7%, it puts things in perspective.

Not to mention, that the way the EU is handling the pandemic, though at the beginning was a disaster, they have been able to control it a lot better than the US has. So given all of these facts, it’s no mystery why investors are feeling safer to park their money in commercial real estate assets in the EU. But let’s further this comparison.

There are many risk factors that real estate investors face when investing, but we are now experiencing several high risk factors. What do I mean by this? We are currently in the midst of a pandemic that is forcing many to work from home, so at the moment office space is not as valuable as it once was. Many also do not feel safe shopping in person and have instead opted to buy things online. This has affected the retail space negatively, but has positively affected industrial space. We also cannot deny the fact that there is a social unrest risk that is definitely higher than what we have seen in more recent years, with looting and destruction of property being a problem in some cities.

Sometimes the truth is hard to swallow, but we can’t deny the fact that the EU has been able to handle the pandemic and the fallout from it a lot better than the US has. Much of the uncertainty consumers in the US are experiencing is coming from the handling of the pandemic. If the US could focus more on containing the virus instead of worrying solely about the economy, we might actually have a chance at getting things back to normal more quickly. It’s a weird position for the US to be in right now to have some many risks in the country, political risk from a possible regime change, social unrest, a major health risk, and because of all of this a faltering economy. You can’t deny the fact that the EU sounds much safer right now.

A Quick Take on the Fed’s New Policies

On August 27th, the Federal Reserve chairman, Jerome Powell, released new policies the Fed would take moving forward, to help stimulate the economy. You can read the whole speech here. The Fed’s new approach is to have maximum employment while also having a flexible use of average inflation targeting. On the inflation side, he has stated that they want to average at a 2% inflation rate. We have experienced an inflation rate of below 2% for quite some time, so this will be an interesting change to come, when we see the Fed manipulating things to be priced higher.

This further control over the economy is eroding the notion that the central bank is an independent entity. I will probably expand more on this and what it truly means on the grand scheme of things in the next blog post. But in the meantime, I’d like to leave you with an opinion piece by Dr. Mohamed El-Erian, the chief economic advisor at Allianz. In it, he states his five key takeaways from the Fed’s new policy change and honestly, I couldn’t have said it better:

As noted by Powell, the changes seek to enhance the central bank’s effectiveness in a “new normal” environment that, in the eyes of Fed officials, has become clearer since the concept was first floated in the aftermath of the global financial crisis. They formalize what has been increasing activism by the central bank to counter the risk of collapsing inflationary expectations and promote employment as a means to making economic recoveries more inclusive while also noting the importance of maintaining financial stability.

Many advocates of Modern Monetary Theory are likely to welcome the new framework as a big step in embracing a policy approach that allows the economy to run hotter for longer, finances large fiscal deficits at low costs and pushes out inflation speed limits on stimulative monetary policy.

This is also why concern is likely to be expressed by those worried about excessive mission creep at the Fed, as well as an erosion in the central bank’s independence and effectiveness. There is also reputational risk in pursuing an operationally more aggressive target after having repeatedly failed to deliver a less-ambitious variant and in formalizing an approach that risks an even wider disconnect between Wall Street and Main Street.

Many in the marketplace will see the new framework as hard-wiring what until now was seen as data-dependent dovishness. This will reinforce the faith investors have in ample and predictable liquidity support, further decoupling asset prices from economic and corporate fundamentals.

Even if deemed necessary to produce superior economic outcomes — in particular, that of sustainably high and inclusive growth without disruptive financial bubbles — the changes are unlikely to prove sufficient on their own. The Fed will remain highly dependent on the ability of successive Congresses and administrations to maintain more pro-growth policies, particularly the pursuit of measures at the intersection of fiscal policy and structural reforms that promote higher productivity growth and lower household economic insecurity.

The more we keep controlling the economy, the more we will end up hurting ourselves in the long-run.

Concluding Remarks

Everything is constantly changing. One minute we have extremely positive economic data coming out and then next we have the complete opposite. It feels like we’re on a rollercoaster and we can’t seem to figure out what will happen next. Like I’ve said in the past, we are currently in the middle of an economic downturn, everything will continue to look and feel like a rollercoaster. The key to staying sane is to look at the longer run. What do I mean by this? Try thinking of all the implications that this economic downturn will have on our future way of life. I gave you a great example with the CEO who isn’t willing to change and adjust, the key is to remain fluid and flexible; think outside of the box. I know many people will tell me that not everyone can do this, but I think we all can, if we look at even the most minute details in our lives. There are ways to become more flexible. Change is inevitable and it’s up to us if we want to adapt or not. I’ve learned this not only works for financial problems, but also for life in general.

Take care everyone and stay safe! I’ll write to you again in 2 weeks.