Written by: Samira Fatehyar

Synopsis

Listen to the podcast version here:

The last 2 weeks has shown us that volatility is still present in the market. It’s hard to not point out that the political risks in the US are rising at levels we haven’t experienced in the recent past. But, like with everything in 2020, the word unprecedented comes to mind. A divisive election is coming up, the Supreme Court Justice seat is trying to be filled before the election, and in all honesty, it feels like it’s one big circus. I keep asking myself, how did we get here? Political risk is what investors are usually worried about in developing countries, not in developed countries like the US. But, here we are.

We’ll start off with looking at newly released economic data. Then, we explore the impending poverty crisis, how it will shape the future, and what we need to do to avoid it. We then jump into the European View, where this week we discuss how Europe is responding to the Covid crisis with Dr. Dimitra Papadovisilaki, an assistant professor of Finance at Lake Forest College.

Economic Update

Chicago Fed National Activity Index

As always when I introduce new measures, I like defining them first so that way we can extrapolate from what the data is telling us. According the the Chicago Federal Reserve, the Chicago Fed National Activity Index:

Is a weighted average of 85 indicators of growth in national economic activity drawn from four broad categories of data: 1) production and income; 2) employment, unemployment, and hours; 3) personal consumption and housing; and 4) sales, orders, and inventories.

Graph 1, below, shows the monthly index from 2018 to now.

Graph 1

Chicago Fed National Activity Index, by Categories

https://www.chicagofed.org/publications/cfnai/index

As we can see from the graph, it’s been extremely volatile this year compared to the previous years. When the numbers are above zero, this indicates an above-average growth rate occurring, whereas a number below zero, indicates a below-average growth rate. If the number is at zero, this means it is on pace with historical average growth trends.

So what we can extrapolate from the graph is that we are nearing the historical average growth trend from quite a volatile few months of being both very below average to being substantially above average in the growth trend. In the latest report, it mentioned that production, sales, orders, & inventories, employment, and personal consumption indicators all decreased. The only category of indicators that increased was industrial production, but even that showed a slowing increase compared to previous months. Housing starts also saw a decline, but more on that in a little bit.

What this index is telling us is that at this moment in time, is that our economic fundamentals are looking to be slowing quite considerably. Does this mean there will be a crash soon? I wouldn’t say that is guaranteed but what I do see continuing is an increase in volatility.

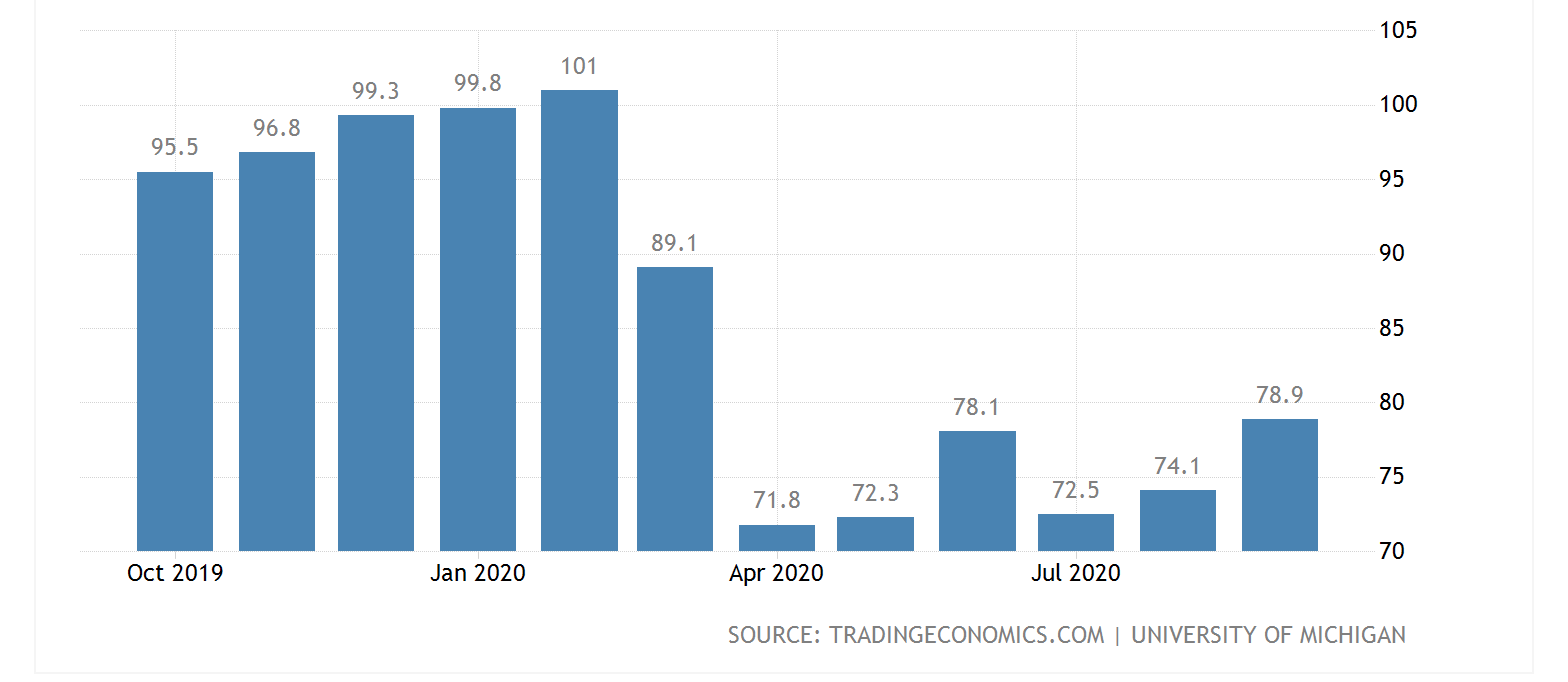

Consumer Sentiment

I always like to look at consumer sentiment and consumer confidence data as it helps us understand the psychology of average consumers. Good news is that consumer sentiment increased to its highest level since March.

Graph 2

Consumer Sentiment October 2019 to September 2020

https://tradingeconomics.com/united-states/consumer-confidence

But now when we look at Graph 2, above, it’s honestly not as impressive, right? Yes, it’s the highest we’ve experienced since March, but it’s nothing to write home about. We increased from 74.1 in August to now 78.9 in September and to put it in perspective we saw 89.1 in March and 101 in February of this year. So, when you think about it, I think it’s pretty safe to say that we are still experiencing a depressed consumer sentiment.

The hope for many retailers is that by the start of the holiday shopping season, we will see much higher consumer sentiment as well as confidence. I will say that it’s been interesting for me to go to Costco in September and see Christmas trees and decor for sale. Since consumer sentiment is psychology based, I think it’s important to point out the affect the holiday season has on all of us. I know that the holiday season brings us all together and gives us a sense of happiness. Yet, the biggest thing that consumes us during the holiday season is the manic consumerism we experience. This is what retailers are hoping for this to happen once again, but with many out of work, I think we will see spending decline. But because it’s a psychology based index, I foresee an increase, all things equal, in consumer sentiment and confidence over the next few months.

Multifamily Starts

New data came out recently highlighting that the amount of new construction in the multifamily sector is starting to decline, granted thought it’s still higher than what it was last year. This does prove just how volatile the market is. Graph 3, below, shows new residential construction as a seasonally adjusted annual rate.

Graph 3

New Residential Construction

https://www.census.gov/construction/nrc/pdf/newresconst.pdf

Multifamily starts declined by 25% from July to August and the amount of new permits for multifamily construction decreased by 17% over the same time period. There are a few explanations for this, one that many will point to is the fact that many construction companies are at full capacity with the projects they have taken on making it hard to take on any new multifamily projects. Another interesting point is that inventory for multifamily may be saturated in the metro markets and since multifamily generally exists in metro areas (where many people are leaving) there won’t be a need to build more for some time.

Another important note to point out is that single family construction has risen by 4% from July to August and has increased by 12% from a year ago. This is especially apparent in suburbs as more people are leaving city centers to live in larger living spaces in the suburbs. Though one could argue that if construction companies were truly backed up with projects they also wouldn’t be able to take on so many single family home construction. Personally, I think the returns on building new multifamily is not near as high as building single family residences and that is why many developers are building that.

Poverty Crisis

K-shaped Recovery

There have been many headlines stating that the inequality in the US is only deepening during the Covid crisis. Many have stated that we are in fact experiencing a K shaped recovery. By definition, a K shaped recovery means that some portion of the population (or sectors) will recover and continue to gain more wealth while the remaining population (or sectors) will continue to decline.

Graph 4

Forecasted K recovery for the US

https://www.uschamber.com/series/above-the-fold/the-k-shaped-recovery-and-the-cost-of-inaction

Graph 4, above, illustrates what the US Chamber of Commerce believes the recovery will look like. To have industries like travel, entertainment, hospitality, and food services needing assistance is not a good sign, especially since there is a large proportion of the population employed in those sectors. I also think that their forecast on retail is dependent upon online sales and the large proportion of the population unemployed and if they will be able to spend or not.

The US Chamber of Commerce also went on to look at the costs of inaction from another fiscal stimulus package. It was estimated that roughly 4 million small businesses have already exhausted their PPP funds and will have to face permanent closure if they don’t receive more money soon. The National Restaurant Association predicts that the industry could lose roughly $240 billion by the end of 2020. US airlines may also be forced to furlough roughly 75,000 airline workers. The impact of inaction is substantial and one that we need to be made aware of. Our growing inequality gap will only multiply if things continue the way they are heading. The American dream may very well be over for many.

Fiscal Stimulus Delay

So what is the hold up on a stimulus bill? Well is multi-fold. To add to the ever increasing bipartisan divide, we are in a very important election year. I think Congress will most likely remain at a standstill until after the election. Congress has become extremely reliant upon the Federal Reserve stepping up to stimulate the economy. But, the Covid crisis is not a monetary issue, it is a health crisis that is leaving millions unemployed. There is a great consensus amongst economists, including Chairman Powell, calling on Congress to help stimulate the economy.

The fact is that the US has only pledged 15% of GDP for fiscal relief whereas Europe is near 30% and Japan is at 40%. And let’s also take into account that we’ve been the worst hit developed nation in the world. Yet, we’re only willing to spend a half than what Europe is willing to spend? It doesn’t make sense to me.

Why isn’t Congress acting? Well, both sides of the aisle aren’t willing to compromise and have been at a stalemate since the program ended at the end of July. There have been rumors of talks continuing between Treasury Secretary Steve Mnuchin and House Speaker Nancy Pelosi, but nothing has come to fruition and, in my opinion, I believe the rumor was to just sway markets in the positive direction on hopes that they’ll reach an agreement soon.

The Republicans are against spending and giving money out to the average American because they believe our national debt is out of control. I agree, but I also think that we need to weigh the costs of inaction or a lesser action for the Americans that are suffering. The Democrats want to spend money and give aid to Americans, which goes with out saying, is direly needed. But, we also need to make sure that the money is getting distributed to those who need it most. The PPP loan program showed just how disastrous government can be with distributing aid.

Now, am I against the government giving out aid? No. Like Chairman Powell, I agree that Congress needs to do more than what they have been doing, which has been arguing. The Fed cannot be the only source of action. Table 1, below, shows government spending as of July 31st, 2020.

Table 1

Fiscal Year 2020 Government Spending, as of July 31, 2020

https://www.usaspending.gov/explorer/budget_function/

Yes, income security is what we spend the most on. But, I see many areas where we can divert money to help this cause, but I’m just a taxpayer and not a representative, so it doesn’t really matter where I think we should divert the spending. The point I’m trying to make is that it can be done if we could have bipartisan agreement, but because we’re in an election year and Congress wants to act like children even more these days, I do not foresee anything getting done until after the election. And who truly suffers? Not the representatives we voted for, but our neighbors. This is what’s so upsetting. Yes, Congress has always been like this, but to be this divided at such a dire time, is frustrating. This wasn’t something the average American could have predicted or even prepared for and yet many will suffer because of the lack of preparedness from our government officials. I will reiterate this once again, we are the worst hit developed nation in the world and yet we’re only willing to spend a fraction on a fiscal stimulus as compared to other developed nations.

My frustration with the way things are going is two fold. 1) The government is in charge of the health response of the pandemic and 2) the government is now deciding to withhold aid to people because they can’t agree and because of how disastrous our health response was in the first place.

Sure, the government has no authority of telling us what we can and can’t do. We live in a free country, right? Correct, but when the health of nation is at stake, I think the collective society has the right to infringe on our individual rights. This follows the same logic the majority was in favor of during 9/11, we were attacked, and then we introduced all these measures that infringed on our individual rights, but it was for the safety of our nation. Whether or not you agree with that logic is a different argument, the point is we have already set the precedent but we’re not following it. Of course, this circles around back to our last blog post with Dr. Clemens Kownatzki, but it’s an important point to reiterate. Why is one different from the other?

Poverty rate

Let’s take a look at what the poverty rate is. Before we begin we should establish the fact that the national poverty threshold for a family of 4 in 2020 is $26,200. The Urban Institute, a think tank that conducts social and economic policy research, conducted a study about what the poverty rate could be during the last half of the year if another stimulus package does not pass. In the study, they mentioned:

However, the federal policy that adds an extra $600 a week to standard UI payments expires at the end of July, and many lower-income families have likely already spent their stimulus money. This means that families with someone still unemployed in August could face increased hardship later this year if additional supports are not provided. The Congressional Budget Office (CBO) currently projects that the unemployment rate will be 10.5 percent in the fourth quarter of 2020 (CBO 2020b), which is three times higher than the unemployment rate in the fourth quarter of 2019 (3.5percent). Further, some people who have remained employed or who were already called back to work are still facing hardship because their hours or salaries have been reduced.

This leads to this discussion of what is the right amount to give people. We want to be able to give them enough to cover their expenses in the short run but also have the ability to save for a rainy day in the longer run. Also, what is the short run? How long do we expect the economic fallout to last? These are all important questions our representatives should be asking and finding the answers to. Of course the longer the fallout lasts, we will witness a higher poverty rate. Sure, everyone has a different opinion on how much is enough, but inaction is more detrimental than not giving enough.

In Graph 5, below, we can see what the annual poverty rate is for 2020 and how the last half of the year will compare if there is no action taken by Congress.

Graph 5

Projected Poverty Rate in 2020

https://www.urban.org/sites/default/files/publication/102605/2020-poverty-projections-assessing-three-pandemic-aid-policies-projections-of-heroes-act-policies-by-race-and-by-state-august-through-december.pdf

From the graph, we can see that there would be a 3% increase in the poverty rate for the whole population if another stimulus isn’t provided from August to December. For those living in a household with a job loss the poverty rate increases by 6.5 points from 9.1% to 15.6%. This is quite high.

Now, many have pointed out that different segments of the population will be hit disproportionately. Table 2, below, breaks down how different races and ethnicities would be impacted by inaction from a fiscal stimulus bill.

Table 2

Projected Poverty Rates in 2020 by Race and Ethnicity

https://www.urban.org/sites/default/files/publication/102605/2020-poverty-projections-assessing-three-pandemic-aid-policies-projections-of-heroes-act-policies-by-race-and-by-state-august-through-december.pdf

What we see from the table above in the All People Category, Black, Hispanic, and Asian American & Pacific Islanders, will end up experiencing double digit poverty rates in the last half of the year. White, non hispanic people will experience a poverty rate change of 37% but will not enter double digit levels. In the category of People in Households with a Job Loss from the COVID-19 Pandemic the numbers shift a bit. All races end up experiencing double digit poverty rates. The highest overall poverty rate would be experienced by Hispanics, then Black non hispanics, then Asian American & Pacific Islanders, and then White non hispanics.

Though percentage changes would tell a bit of a different story. Since Hispanics already experience a higher poverty rate for those who live in a household with a job loss from the pandemic the percentage change for them is actually the lowest at 55%. The highest in the change is Blacks, then Whites, then Asian American & Pacific Islanders, and then finally Hispanics. It’s quite interesting when we break it down. But regardless, these are still record high numbers and not ones we should brush off.

In Comparison

So how does this compare with previous downturns we’ve seen? I truly believe it’s hard to compare the Great Depression of 1929 poverty rates with what we are currently seeing because there has been many technological advances since then. Though for those interested, the Great Depression saw poverty levels at and around 50%.

But if we look at the Great Recession we see a similar trend to what we may start witnessing soon. The Metropolitan Policy Program at the Brookings Institute, a think tank that conducts research and provides policy analyses for new problems arising in the economy at the city and metropolitan levels, conducted research in 2010 that provided insight on the poverty rates during the Great Recession. In their study they found:

Between 2007 and 2009, the national poverty rate rose from 13 percent to 14.3 percent, and the number of people below the poverty line jumped by 4.9 million. Yet because the economic impact of the Great Recession was highly uneven across the nation, the map of U.S. poverty shifted in important ways over the past couple of years, with implications for both national and local efforts to alleviate poverty.

It’s interesting to note that once again we are experiencing a recession that is having uneven effects across the nation, not only geographically, but also racially and socioeconomically. The highest poverty level observed due to the effects of the Great Recession was in 2011 which saw a poverty rate of 15%. In another research paper written in partnership between The Russell Sage Foundation and The Stanford Center on Poverty and Inequality on October 2012, they found an interesting characteristic between recessions and the poverty rate.

In the recessions of the early 1980s and early 1990s, the poverty rate was also approximately 15 percent, even though these were more moderate downturns. The poverty rate did not increase more in the current downturn in part because of federal stimulus spending.

Just for clarification, when they refer to the current downturn they are referring to the Great Recession. But from what we have seen in the past, it’s not unusual for the US to see a poverty rate of 15% during economic downturns. This provides us with an interesting realization in that we are currently seeing high poverty rate numbers, but they are not at 15% yet, which implies that either the worst is yet to come or that this economic downturn will not be as bad as previous ones.

I would add that we won’t know official poverty rates numbers until next year, so we should take this with a grain of salt. We have a number of moratorium that will eventually be ending as well and that will obviously change many things, especially if another fiscal stimulus bill isn’t passed.

European View

A Comparison and contrast between Europe and the US

A Conversation with Dr. Dimitra Papadovisilaki

Before I begin, I want to mention that Dr. Dimitra Papadovisilaki and I first met when she was my professor of monetary economics during my undergraduate years. We then became very close colleagues and discuss current economic events often. She is currently on sabbatical in Greece and I wanted to get a sense of what she is currently experiencing in Europe and how it compares to what we are experiencing here in the US. We had an interesting conversation about the differences in the responses of the EU compared to the US response to the Covid-19 pandemic.

Before we begin, I’d first like to give her a brief introduction. Dr. Papadovasilaki is incredibly knowledgeable in the fields of behavioral and experimental finance, financial crises, and applied macroeconomics. As a professor, she challenges her students to think critically. As a colleague, she can play devil's advocate and easily challenges the views others have. She has published a list of papers all relating to behavioral finance and macroeconomics. She is from Greece and has an impeccable understanding of the European Debt Crisis. Dr. Papadovasilaki is currently an Assistant Professor in Finance at Lake Forest College in Illinois. To listen to the interview, please check out the podcast. The following is a transcript of our conversation.

Samira: Thank you for being here, Dimitra. I know there is a big time difference in addition to some internet complications but thank you for agreeing to come on and talk to us.

Dimitra: Thank you for hosting me, I’m very happy to be with you. It’s a very nice moment to have your student thriving and being apart of it, so I’m very happy to be here.

Samira: Aw, thank you so much! So since you’ve lived in both the US and Europe, you’ve seen and experienced many events first hand, including the Covid-19 pandemic. What have you witnessed in terms of the government’s health response to the Covid-19 pandemic, both in Greece and Europe in general?

Dimitra: So I spent the biggest part of the lockdown in the US, I was there until July and I arrived in Greece in July. But of course I knew what was happening here. So the main difference was the response in terms of organization, there was a common response to the Covid outbreak from the European Union, an organized one, a very responsible one. While, in contrast in the US, I would say it was completely chaotic, unorganized, irresponsible, and criminal based on what we saw over the last month in terms of when the knowledge about Covid was available to the administration. So we see that Europe started the lockdown very early on, very fast, imposed strict lockdowns basically, mandated mask wearing, while we’re still discussing that in the US, and we see Covid rates going up and we don’t see improvements. Of course, we do have a second wave right now in Europe and things are starting to become different than it was before, like earlier in June. However by making simple comparisons, you can see still the US is handling the situation very wrong and bad. For example, Greece is a very small country and has a population of about 10 million people and in comparison the state of Illinois has about the same population, about 12 million or 12.5 million, and the total number of Covid cases in Greece is 16,000 whereas for Illinois it is 289,000. And then we talk about 356 deaths in Greece versus 8,826 deaths in Illinois at least the last time I checked which was yesterday (9/26/2020). So you see immediately, in contrast, a huge difference that I think has to do with the administration.

Samira: That’s a very interesting observation that you’ve seen. What are some of the major differences between the healthcare systems between the US and Europe, for our listeners that are skeptical about the healthcare system in Europe?

Dimitra: They shouldn’t be very skeptical about the healthcare system in Europe; I’m not saying that it doesn’t have flaws, don’t get me wrong. But, we are talking about two completely different healthcare systems. So the US doesn’t have a universal healthcare system; we are talking about health insurances. There is no provision for public health, basically, if we want to be pragmatic, there is not. I still remember when my husband and I were fresh in the US, we were in our first semester in the US, he dislocated his arm. We were at the University of Nevada, Reno and we thought we should call the ambulance, which is what you would do in Greece. When you do that in Greece, you don’t have to pay anything, you just call the ambulance and they take you to the emergency room. We did the same thing in the US and then they told us that we have to pay roughly $1,700 and we didn’t know what was happening. We were wondering if they mixed our bill with something else. It was completely insane for us that we had grown up in a universal health care system and again I’m going to say that it has its flaws, of course. However, I believe that health should be a public good and should be provided to everybody. Especially, when we are talking about a country with such a huge inequality. And the fact that we have these vast differences talking about the universal healthcare system in Greece and in the majority of European countries, versus a privatized healthcare system, also contributed to the Covid rates. Basically, healthcare in the US is business and it shouldn’t be. Health should be equally distributed to everybody. Now, because of the high cost, especially in drugs, that the US has, based on various studies, there are lots of individuals that are skipping medical examinations because they don’t have to pay. Given that they don’t have to pay, they result in bad health and conditions that unfortunately, being affected very badly from Covid. So this is another factor to take into account. The access to the healthcare system was not distributed equally. We are talking about pure efficiency in the US, not in equality and you see that in the number of ICU beds, physicians that were available, in the drugs that could be produced, I mean at some point, basic things were not existing. So this is a big difference and the sad part is to see how different groups of people are being affected by Covid and I’m talking about discrimination that results in wealth and income inequality and that’s a consequence. For example, in Chicago, at some point in the Spring, 70% of those that died by Covid were Black people. This is outrageous. And this has to do with the fact that there is no public provision for health. Again, I’m going to say that, having grown up in Greece, I know that there are flaws and negative externalities with public health but there are many things we can do to internalize these externalities and not go to an extreme case of privatizing the health care.

Samira: So, basically you’re saying there is better preventive care in Europe?

Dimitra: Yes, there is access to preventative care. For example, an acquaintance of mine was also surprised by the provision of drugs. That acquaintance was diabetic and was taking insulin and had to pay for insulin in the US and went as an exchange student to Germany and there insulin was provided for free. And that was like something that would have never been imagined. In general, the healthcare differences are so vast and people and people don’t really know about them. Now with Covid and the conditions we are experiencing, I see Europeans realizing how the system works in the US.

Samira: That must be a big reality check for them to realize it’s not the same.

Dimitra: As what happened to me, when we came to the US and called the ambulance.

Samira: Right, that makes sense. What are some of the key differences in the fiscal policy response that you’ve seen in Europe and the US?

Dimitra: So, the Eurozone consists of 19 countries. The European Union, with Brexit, is 27. We are talking about countries that are very different economically speaking and culturally speaking. The structure of each economy is different. The Greek economy is based on service and heavily dependent on tourism. For example, that’s not the same in Germany. Germany is based more on manufacturing. Germany has an accumulation of budget surpluses and ultra low interest rates for borrowing whereas Greece has been fighting, unfortunately, over the last decade with a debt crisis and doesn’t have the same power, doesn’t have the same tools for fiscal policy as Germany. So you see differences in the responses among the countries. Germany spent a lot of money for keeping consumption and not having decreases in the rates of consumption, which is also part of the fact that they could handle thing very well with Covid, on top of having the ability to handle consumption and keep up household confidence with consumption basically. The German economy spent a lot of money in subsidizing furloughed employees. In this case we wouldn’t talk about laying off people, but basically subsidizing the companies, pay the companies to pay the employees which made it much easier to keep people employed. And Germany, as of now, is looking to a V-shaped recovery, of course we don’t know too much until we see what happens with the second wave. But the original contraction for Germany, in terms of GDP, was 6.3%, but as of the latest data it was 5.8%, so they were projecting it to be worse than it actually is. And that has to do with how the economy was. Greece has been suffering, on top of the debt crisis over the last years, by very high rates of unemployment. Until recently in 2018, the rate was above 20%. We are starting from a different basis of course. On top of that, the international creditors would lend to Greece with the premise of turning the debt into sustainable debt. And their idea of turning the debt into sustainable debt was through government spending cuts, heavy cuts and an increase in taxes. Which contradicts what we were trying to do. The debt to GDP ratio will go up when GDP doesn’t grow and GDP cannot grow when you have high taxes and government cuts. So, over the last decade, there was an improvement in the numbers at least in Greece, but not what it should be if it was done differently. So the goals and the fiscal tools that were used were completely opposite. And nevertheless, Greece did try a lot with Covid right now and had an early lockdown resulting in low rates of Covid at least until June and then we had the opening of the borders for tourism. So Greece spent less money in comparison to Germany. However, they did take some measures and they cut some taxes, they subsidized rents, they are giving subsidies to sectors that were hurt the most and in certain areas more. They provided some payments to those who were unemployed and it wasn’t enough.

Samira: So how does this compare to what we know about the fiscal response in the US?

Dimitra: A difference for example with the US was unemployment benefits. Instead of giving unemployment benefits, they should have given the opportunity for employees to remain employed and subsidize their payments through their employers. Then we had the issue with the small businesses that could not access lending in the US, lots of the businesses could not cover operating costs for more than 10 days. The whole process was very difficult and the money wasn’t enough for all businesses. So it was not as quick. And again, we should be talking about each European country differently.

Samira: That’s very interesting to see that even within the European Union there are different responses in fiscal policies and then seeing how that compares to the US. I mean, they’re all so very different in how they handle the crisis, which I find really fascinating. So, along the same lines, what are some of the key differences in the monetary policy response that you’ve seen between Europe and the US? And of course we’re talking about the European Central Bank and the Federal Reserve in the US.

Dimitra: The Federal Reserve in the US, I think, responded very fast, very well, and took responsibility in going to the extreme. They took extreme measures. More extreme than what we saw in 2008 with quantitative easing. I think this partially explains what we’ve seen in the stock market in the US. That the Fed is keeping up the confidence to a certain degree. The European Central Bank works differently than the Fed and one of the reasons is structural. We are talking about different countries, not the same nation as is the case with the Fed. However, right now, even since the outbreak started, the European Central Bank did take different measures than it had at least during the bad years that Greece experienced. And by that I mean that the European Central Bank implemented the pandemic project, the PP. The Pandemic Emergency Purchasing Program, that is basically a form of quantitative easing of putting money in the economy and in the past Greece could not be part of it, due to the ratings of the bonds. This was a problem because Greeks would have to borrow at much higher rates. Right now this is giving some help in the Greek economy and potentially it might be a starting point for doing things differently, in a more unified approach.

Samira: That’s interesting so it looks like some countries benefit more from more monetary policies as compared to fiscal policies and some countries benefit more from fiscal policies as compared to monetary policies.

Dimitra: And also the type of events. Expansionary monetary policy is a tool you should be using in extreme times and this is an extreme time. The Greek debt crisis was an extreme time and they shouldn’t had let the country suffer so much.

Samira: And while we’re talking about that how would you say the Covid crisis compares to the European Debt Crisis in Europe and then also in Greece, more specifically? I know you have many personal stories with that. I remember in your class, Money and Banking, we heard a lot about the personal stories behind the European Debt Crisis and it made it more of an experience for me especially because it was like people were suffering at that time. Where we don’t usually see that on the news, it’s just like Greece is broke and that’s about it, you don’t see the actually suffering of the people. So I want to know how does this crisis that we’re going through right now compare to that crisis?

Dimitra: So the economy was recovering very slowly over the last three years, we could say. At least the numbers were improving and the numbers are not generally translated with people’s feelings. For example, I told you that unemployment dropped after 2018 to about 17%. GDP grew between 2013 and 2019 by 5.5%. We did have some improvements and things were looking a little better and with Covid things will be, well it depends on the way we see the future, there is so much uncertainty right now, in terms of the second wave and what we are going to see. The expectations are that the GDP is going to have a drop of about 10% for this year. And of course the spending that took place for Covid will add to the debt. However, if we see things as they really are and understand that austerity doesn’t really give you what you are looking for that will give a different turn. A good thing that is happening right now is that the European Union has made a deal on a post-pandemic recovery. That means 72 billion euros will be allocated for the recovery, which is a very good starting point, hopefully for the best. Now, what’s going to happen in terms of the debt later, again, that is something we should discuss after the second wave, after we see the response of the European Central Bank and after we see what’s happening with quantitative easing. I’m afraid that if we don’t understand that there is a need for a more unified approach in solving the problem, we might have potentially austerity measures again in two years and get back to a vicious cycle, but that’s something that remains to be seen.

Samira: So there is a lot of uncertainty and most likely volatility.

Dimitra: And we’re talking about people that have suffered for so long. We are talking about unemployment rates that are insane. People are leaving the country to work abroad and people that have the tools and the abilities, it’s very sad.

Samira: Yeah, I mean when you mentioned 17% unemployment rate, that’s insane for us.

Dimitra: That’s the improvement, right? And that’s based on the fact that many people have left to go abroad.

Samira: That’s a very interesting observation that you can tell us about.

Dimitra: And unemployment is going to increase, now with tourism because the government had to close the borders and tourism started late. And of course with tourism, the rate started to going up tremendously. Right now a big number of people were laid off because of the conditions which makes sense, you need to put health first. If we were all more careful and more considerate about each other, wear masks, and keep our distances the economy would be able to recover faster because we wouldn’t have second waves or third waves.

Samira: And that advice really goes for all countries, the economic recovery is hinged on the fact that we can control the virus. I think a lot of the time people forget that, so it’s really good to see that you’re also reiterating that point. So I do have one last question, do you have any advice you’d like to share with our listeners?

Dimitra: I do think we should be very empathetic with each other. Remember that we’re talking about lives here and the fact that one’s life is not in danger because they don’t have underlying conditions or they are young doesn’t mean that we can put other people’s lives in danger. We should be empathetic. We should wear a mask. We should keep our distance and try for the best.

Samira: Thank you Dimitra! I really appreciate you coming on and I look forward to having you on the show again.

Dimitra: Thank you very much, it was very nice to be here. I wish you all the best!

Concluding Remarks

Whether you support Trump, Biden, or a third party candidate, I think we can all agree that something needs to be done to help our fellow Americans who are struggling. Sure, there are different ways to achieve this, loans vs handouts and so on, but the fact is something needs to happen.

As we continue to inch closer to the election, I can’t help but feel like we’re all waiting for this grand finale moment. That somehow after the election the pandemic will disappear, the economy will roar back, and the VERY deep political divide will dissipate. The only way to achieve this is for all of us to work together to get there. But one can only remain hopeful, right?

Take care everyone. Continue to stay safe and healthy! I’ll write to you again in 2 weeks.